Few members of Congress are considered more liberal than Barney Frank. Gay, left-handed, and Jewish, as his biography’s title proudly proclaims, he clearly enjoys living in direct contravention of right-wing ideals.

A favorite conservative punching bag, Glenn Beck and Bill O’Reilly have their tea party base convinced that it was actually Frank who sent the country into an economic tailspin, through some curious combination of incompetence, redistributive zeal, greed, and homosexuality. Beck’s conspiratorial chalkboards link Frank to the mortgage giants Fannie Mae and Freddie Mac, back to the community organization ACORN, and by implication, to the poor and undeserving. Naturally, liberals have responded by closing ranks around the congressman.

The pseudo-research of Fox News and friends, and their obsession with Fannie and Freddie -- hardly the root of all economic troubles -- have distracted from a core reality of Frank’s recent career in Congress. Since becoming the ranking Democrat on the House Financial Services Committee seven years ago, he has built a formidable Wall Street donor base, even by Washington’s standards; as the housing bubble grew, so too did his fundraising purse and his stature, in Congress and beyond.

In the course of this Wall Street-fueled fundraising blitz, Frank developed a web of relationships, alliances, and attachments to financial elites that have repeatedly undermined his independence on everything from bailout negotiations to the financial reform legislation that he recently shepherded through the House. And his friends in finance continue to extend -- and collect on -- their investment.

Frank on 'FIRE'

On one day in late July of this year, the Weiss family of Brookline, Mass. gave a whopping $24,000 to Barney Frank. He received maximum contributions of $4,800 each from Kara, an MFA student in Seattle; Judith, an undergraduate at UC Davis; Danielle, a psychology PhD at Tulane; and their parents, Bonnie and Andrew. (All campaign finance data is drawn from OpenSecrets.org and LittleSis.org.)

The Weiss daughters, who had previously given a grand total of two $250 contributions, would seem to be unlikely top contributors to Frank. But their father Andrew is a hedge fund manager, and therefore a key constituent of the powerful chairman of the House Financial Services committee.

Joining the Weiss family in funneling Wall Street dollars to Frank that day were two other hedge fund managers, Eric Vincent and Michael Inserra, and former Republican Congressman Richard Baker. Baker is president of the Managed Funds Association (MFA) -- the hedge fund industry’s main lobby -- and Inserra and Vincent are both board members.

Baker had testified before Frank’s committee just ten days earlier on the financial reform package snaking its way through the House. The MFA PAC cut Frank a $10,000 check a few days after the testimony.

By the time the House of Representatives passed financial reform legislation on Dec. 10, the bill reflected one of the hedge fund industry’s main asks -- lax oversight of the financial instruments known as over-the-counter (OTC) derivatives. After the bill passed, financial analyst Chris Whalen told Bloomberg News that “the OTC reform has gotten to be basically irrelevant as far as change… compared with what we thought we were going to get over the summer, it’s night and day.”

Meanwhile, Frank supported Wall Street and the hedge funds on at least two points where they lost out. He opposed an amendment offered by Brad Sherman that forces hedge funds to pay into a systemic risk fund; it passed with the overwhelming support of the committee, 52-17. A bipartisan measure to audit the Federal Reserve also passed without Frank’s support.

The final bill was barely out of the House before Frank was on CNBC, claiming victory but cautioning that the Fed provision -- the most celebrated populist measure in the bill -- threatened the institution’s “independence.”

Maybe the Weiss family’s contributions had something to do with Frank’s lukewarm support for more substantial reforms. Or Baker’s, or Vincent’s, or the MFA’s. Or those of any one of the deep-pocketed Wall Street supporters that Frank has cultivated since rising to a leadership post on the financial services committee.

For years, Frank was a mediocre fundraiser. In 2002, he was ranked 185th out of 215 Democrats in the House in total fundraising take. Previous years were similarly unimpressive.

That all changed in late 2002, when he became the most important Democrat on the financial services committee, replacing Rep. John LaFalce. In the following election cycle, Frank increased his fundraising five-fold, from $268,000 to $1.4 million. He cruised to re-election, though Democrats failed to take back the House that year.

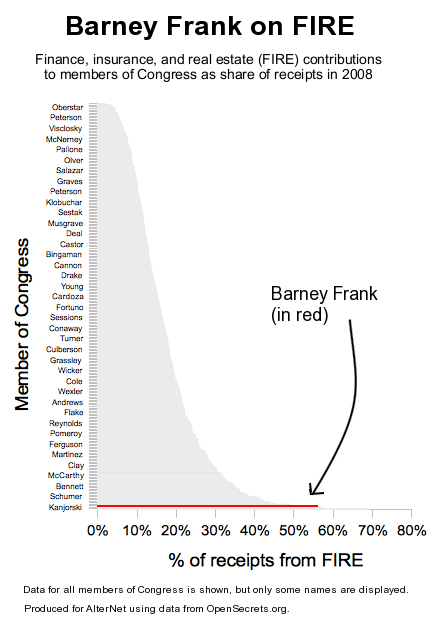

Due to his leadership of the finance committee, Frank derived the greatest share of his cash, and his newfound power, from Wall Street. He consistently raised more than 50 percent of his campaign contributions from the finance, insurance, and real estate industry, often referred to as “FIRE” -- essentially the bundle of interests that had the most to gain from the housing bubble. By contrast, before becoming ranking Democrat, the FIRE share of his money hovered around 25 percent.

Remarkably, only two members of the House have taken in a larger share of their money from Wall Street over the past two campaign cycles -- Paul Kanjorski, a Democrat, and Spencer Bachus, a Republican. And during the 2006 cycle, Frank took in more money from FIRE than any other Democratic member of the House, and all but a few Republicans.

In 2009, Frank has taken in 48 percent of his contributions from FIRE, more than $400,000. Only one Democrat, Jim Himes, has raised more from Wall Street. Melissa Bean, that darling of Wall Street, actually trails Frank by several thousand dollars.

To put Frank’s funding mix in perspective, for every 20 Wall Street donors calling his office, there are two union presidents, one healthcare executive, and a handful of activists and business executives in other industries. (Check out this awe-inspiring graph, to grasp this more fully.)

{kind=link}

With all that big money behind him, it's no wonder Frank has gone virtually unchallenged in his recent electoral campaigns. And he has used his Wall Street war chest to fund other Democrats across the country, building his influence and power within the party. It is that power, both symptom and cause of his chairmanship of Financial Services, that made him the Democratic Party’s point man on the financial crisis in fall 2008.

For clues as to how Frank got there, we can look to Representative John LaFalce, Frank’s predecessor as the ranking Democrat on the House Financial Services Committee, who was similarly dependent on FIRE.

In 1999, LaFalce was credited with being a key force behind landmark legislation in the history of financial deregulation -- the Gramm-Leach-Bliley Act.

GLB, as it is known, tore down the walls between commercial and investment banks set up by the Depression-era Glass Steagall Act, paving the way for the creation of too-big-to-fail behemoths like Citigroup. Democrats were in the minority at the time, so LaFalce wasn’t chair of the House Financial Services Committee, but he was credited with making sure the financial modernization bill was of high priority to the Clinton administration.

Soon after the legislation passed, LaFalce and other key policymakers reveled in their victory by gorging themselves on a cake bearing the epitaph of Glass Steagall. And then there was LaFalce’s retirement party, in 2002, where two lobbyists representing Bank of America, Morgan Stanley, and other financial interests sang a humorous tribute named “Big John.” LaFalce hailed from western New York, a region hit hard by financialization and de-industrialization, and far from the area he truly represented: Wall Street.

The staff is where it's at

Frank gladly inherited LaFalce's legacy. The Democratic wing of the financial services committee was still open for business. He indicated to the press that the Gramm-Leach-Bliley Act would not be re-considered, and he would keep key members of LaFalce’s team, including senior counsel Lawranne Stewart and chief of staff Jeanne Roslanowick.

By relying on Stewart and Roslanowick during the unfurling of the financial crisis, Frank has looked to the very enablers of the recent financial catastrophe to remedy the current situation. Both staffers played key roles in shaping the Clinton-era financial reforms that drove the U.S. economy to the brink last year. And as Frank negotiated bailouts and steered financial reform legislation through Congress, they’ve been two of his top lieutenants.

Roslanowick’s various biographies give her credit for playing an important role in crafting GLB, and LaFalce described her as “tough as nails and absolutely unyielding” in negotiations on consumer protections and community reinvestment. But it is unclear which policy questions she held her ground on as the bill’s sole achievements for consumers were toothless privacy reforms and ATM fee notifications, and its most significant community reinvestment provisions were attempts -- authored by GOP Sen. Phil Gramm -- to embarrass community groups.

Granted, it could have been much worse -- Gramm wanted to end the Community Reinvestment Act (CRA) altogether -- but this was certainly not a consumer-oriented legislative achievement to hang one’s hat on. Consumer advocates called the GLB a massive giveaway to Wall Street, and Public Citizen would spend the next decade pointing to the negative effects of banking consolidation brought about by the bill.

In financial reform’s most recent iteration, Roslanowick and company appear to have forfeited on CRA once again. The bill gives the Consumer Financial Protection Agency no oversight of financial institutions on CRA issues.

Roslanowick’s fellow LaFalce/Frank staffer, Lawranne Stewart, has an embarrassing history with the financial products known as derivatives that the bill was supposed to address.

Stewart, now senior counsel at Financial Services, helped author the Clinton-era legislation that cleared the way for the great derivatives explosion of the Bush years, which eventually brought AIG to its knees in September 2008. From 1999 to 2001, she was Undersecretary of the Treasury Gary Gensler’s top lieutenant, and helped craft the legislation known as the Commodity Futures Modernization Act. In March, Senator Bernie Sanders put a hold on Gensler’s nomination as chair of the Commodity Futures Trading Commission, over concern for his role in shaping that legislation. Gensler was eventually confirmed, and has established himself as a tougher critic of Wall Street than was expected.

Stewart’s authorship of that legislation is evident in this celebratory email between Enron lobbyists sent on December 12, 2000.

Stewart passes the document containing “an amendment to the definition of ‘trading facility’ to exempt single dealer markets” along to her boss Gensler, who then forwards it to the lobbyist George Baker with the subject line “as discussed.” Baker then forwards it to derivatives lobbyist Ken Raisler, who then forwards it to Enron lobbyist Chris Long, who then passes it along to the rest of Enron’s lobbying team with a brief analysis, closing with: “They may cut a deal as early as this afternoon!”

Elements of this bill would later become known as the “Enron loophole,” which exempted energy trades from proper oversight and were believed to be behind historic spikes in fuel prices during the spring and summer of 2008. Though Democrats have blamed Senator Phil Gramm for the loopholes, Enron lobbyists were actually worried that Gramm would hold out for something too radically deregulatory, thereby putting their sought-after language in jeopardy. In any case, a compromise was reached, and Stewart played a key role in crafting the Enron-approved language.

Ironically enough, Stewart’s considerable personal fortune is derived from the murky world of international energy privatization, which Enron dominated until its demise. Her husband, Mark Kantor, worked in that field as an international project finance attorney at the law firm Milbank Tweed during the nineties. Milbank Tweed worked closely with Enron on numerous energy deals and off-balance-sheet financings, to the extent that the University of Calfornia filed suit against the firm in 1999. Kantor himself worked on at least one Enron-owned project, a Turkish power plant named Trakya Elektrik.

Indeed, the derivatives market reforms passed by the House this month look like they were written by an Enron attorney; the legislation exempts “end users,” a classification that loops in speculative financial engineers like Enron.

Two other Frank staffers passed through the Wall Street-D.C. revolving door in 2007 and 2008, but in opposite directions. His special counsel, James W Segel, lobbied for the Investment Company Institute, a mutual fund lobby, for ten years before joining Frank’s staff. Board members of ICI include representatives of Goldman Sachs and JP Morgan.

Michael Paese, Frank’s deputy staff director at the financial services committee until 2007, is now a registered lobbyist for Goldman Sachs. He has been lobbying Congress on issues related to financial reform for the past year. At least two other top Frank donors, Mitchell Feuer and Michael Berman, also lobby for Goldman Sachs.

Indeed, Frank’s ties to Wall Street are in evidence whenever he goes on television to articulate his vision for dealing with the financial industry. Bailouts help individuals, not companies, he told 60 Minutes, before accusing the host of attacking welfare and wanting to see people starve. After we bail the banks out, then we can tax them, he told Ed Schultz, who was criticizing the bailouts in a manner that Frank found “condescending.”

He may have a silver tongue, but Frank’s quips over the past year have sounded less than persuasive and more like the defensive posturing of a liberal beholden to Wall Street’s big money.

Can he be a good friend to both sides?

Last Wednesday, Rep. Melissa Bean and a coalition of New Democrats held up the financial reform process in order to win key concessions for Wall Street. Frank criticized her opposition, pointing to the influence of big banks, and entered a meeting with Bean and other leaders of the House.

Frank emerged, after about an hour, remarking that “the differences have been narrowed, and I think you’re getting something that both sides can live with.”

What were the two sides, exactly? Presumably, Frank counted himself among the reformers. But how could someone so dependent on Wall Street for fundraising dollars present any meaningful opposition to the financial industry’s agenda? Any tug-of-war inside that chamber would have consisted of everyone pulling in one direction, and all falling down.

The brief negotiation was certainly successful. Bean got what she wanted on derivatives regulation and federal preemption of state law. Frank got to pass a historic financial reform bill, all the while retaining his power as one of Wall Street’s chosen in Congress. The political theater was reminiscent of the great bailout negotiations of 2008, in which Frank and his liberal friends conceded hundreds of billions of dollars to the sinking Street.

The truly remarkable thing about the Barney Frank phenomenon is that liberal advocacy groups continued to treat the Congressman as an ally during the financial reform process. Public Citizen issued a press release that criticized parts of the bill, but thanked Frank for his work. Marcy Wheeler of Firedoglake called him a “good progressive,” fighting the good fight against banking interests. ActBlue, the progressive political action committee, is Frank’s biggest donor this cycle.

Meanwhile, Frank has spent much of the last seven years cultivating relationships with individuals like Richard Baker and Andrew Weiss, Wall Street executives and lobbyists who leverage their influence to game the democratic process. The Weiss family and its hedge funds have actually outspent ActBlue on Barney Frank this cycle -- all during that fateful summer of 2009, when meaningful derivatives reform was still on the table.

The numbers don’t lie. Forget Fannie or Freddie -- Wall Street owns Barney Frank. He has been lifted to power by the entire class of Wall Street financiers that brought the U.S. economy to the brink.

Why should he abandon them now?

Report typos and corrections to: feedback@alternet.org.

#story_page_sidebar

MOST POPULAR

{{ post.roar_specific_data.api_data.analytics }}

MOST POPULAR

ContactAdvertise with AlterNetPrivacy PolicyWriter GuidelinesPress InformationAbout AlterNetMeet the AlterNet StaffDebug Logs

@2026 - AlterNet Media Inc. All Rights Reserved. - "Poynter" fonts provided by fontsempire.com.